America’s Health Insurance Crisis in Six Charts

Rising costs, soaring profits, inadequate coverage, and crushing debt.

Michael Mechanic

Earlier this month, the Commonwealth Fund published the results of its biannual survey on the state of health insurance coverage in the United States. Good timing, given the recent uproar over the business conglomerates that dominate the sector and seem to be more concerned with maximizing investment returns than ensuring the health and wellbeing of their customers.

Despite the Commonwealth Fund’s mission—to “promote a high-performing, equitable health care system that achieves better access, improved quality, and greater efficiency, particularly for society’s most vulnerable”—its agenda is decidedly nonpartisan. I recently talked to a doc from Physicians for a National Health Program who made a good case for abolishing for-profit insurers entirely.

Commonwealth doesn’t quite go there. Although the survey report says public options should be made available, the primary policy recommendations involve bolstering Medicaid, the federally funded public insurance program for low-income Americans (the incoming administration appears likely to do the opposite)—and protecting consumers from medical debt. (Ditto.) But the findings “show pretty clearly that commercial insurance is not enabling timely and affordable access to health care without fear of medical debt for millions of people,” one of the authors, Sara Collins, told me in an email.

Indeed, it’s hard to look at these six charts—five of which are derived from the Commonwealth report—and not conclude that something is rotten in Washington and on Wall Street. The Affordable Care Act, which Republican lawmakers very nearly repealed during the first Trump administration, has cut the number of uninsured Americans in half, to 26 million last year, or roughly 1 in 12 people. (This number will certainly rise if Congress fails to renew enhanced ACA premium subsidies put in place during the Biden administration, which are set to expire in 2025.)

But when you factor in the number of underinsured Americans and the number of people carrying medical debt, even the current state of health coverage is far from ideal. The Commonwealth surveys were conducted this spring with 6,480 people, ages 19 to 64, who for the most part rely largely on commercial plans obtained through their work or via the ACA exchanges.

It also turns out that even being insured (and not underinsured) doesn't leave you in the clear. ("We don’t use the term 'fully insured,'" explains Collins.) The term "underinsured" is for people whose annual out-of-pocket costs (not including premiums) add up to more than 10 percent of their household income—or half that for a family of four that makes less than $60,000. You are also underinsured if your deductible, the amount you have to pay before coverage kicks in, is at least 5 percent of your household income. Growth in the number of underinsured people, Collins notes, "has been driven by growth in the proliferation and size of deductibles, especially in employer plans."

According to the Kaiser Family Foundation, average annual out-of-pocket medical costs, adjusted for inflation, have more than doubled since 1970, to $1,425 per person in 2022. And remember that healthy people don't pay nearly so much. It's the sicker folks who face the high out-of-pocket costs. In fact, roughly a quarter of insured people with certain chronic health conditions said they were skipping doses of medications their doctors prescribed, or hadn't gotten prescriptions filled, because of the cost.

Given the above, it shouldn't be surprising that lots of people who thought they were adequately insured have found themselves in debt to hospitals, medical and dental care providers, financial institutions, and bill collectors. The numbers are, of course, higher for uninsured and underinsured people.

The sums are not paltry, as the Commonwealth survey found. More than one-fifth of the people with medical debts owed at least $5,000.

And as anyone who has been in such a situation knows, the albatross of debt puts a serious crimp on a body's well-being.

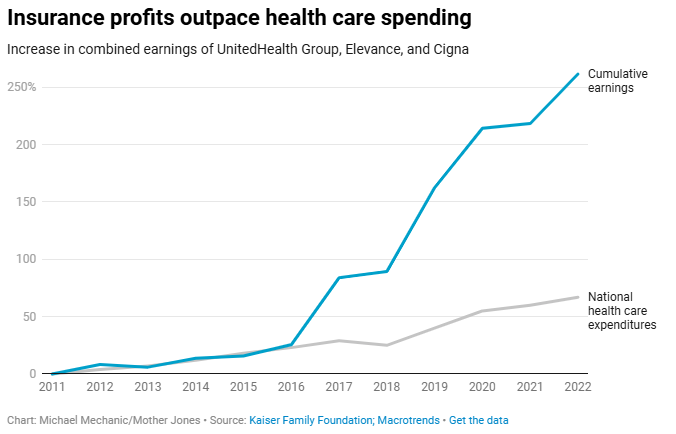

But hey, at least somebody is doing well: executives and shareholders.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.